No single vendor dominates all of IAM — but a few clearly own their respective layers, and those positions are more durable in some categories than others. If you're evaluating the market either as a buyer or as someone trying to understand where investment is going, the useful frame isn't "who wins IAM" but "who leads each layer and how sticky is that lead."

The practitioner consensus from this thread is worth taking at face value. The breakdown by layer is accurate and reflects how identity programs are actually structured in enterprise environments.

How the IAM Market Breaks Down by Layer

Directory and workforce identity: Microsoft Entra ID. Microsoft's position here is essentially permanent for any organization running M365 and Azure. Entra ID is the identity fabric for the Microsoft ecosystem, and the M365 installed base is so large and so sticky that displacing it would require replacing the entire productivity stack. Active Directory on-prem is similarly entrenched in hybrid environments. Microsoft's dominance in this layer isn't at risk from any current competitor — it's reinforced with every M365 renewal.

SSO and access brokering: Okta. Okta built its position on two things: the largest app integration catalog in the market and a cloud-native architecture that enterprises adopted before Microsoft's cloud identity story was fully formed. That position is more competitive now than it was five years ago. Microsoft Entra is increasingly capable for Entra-heavy shops. Ping Identity (now merged with ForgeRock) has enterprise traction. But Okta's integration breadth and its position as the neutral IdP in mixed-cloud environments keeps it relevant in stacks that aren't fully Microsoft-aligned.

Privileged access management: CyberArk and BeyondTrust. CyberArk's acquisition of Venafi extended its reach into machine identity alongside its established PAM position. BeyondTrust leads in endpoint privilege management and remote access. Delinea (the Thycotic and Centrify merger) competes in the same space. This layer is dominated by incumbents with deep enterprise roots and is unlikely to see significant market share movement in the near term.

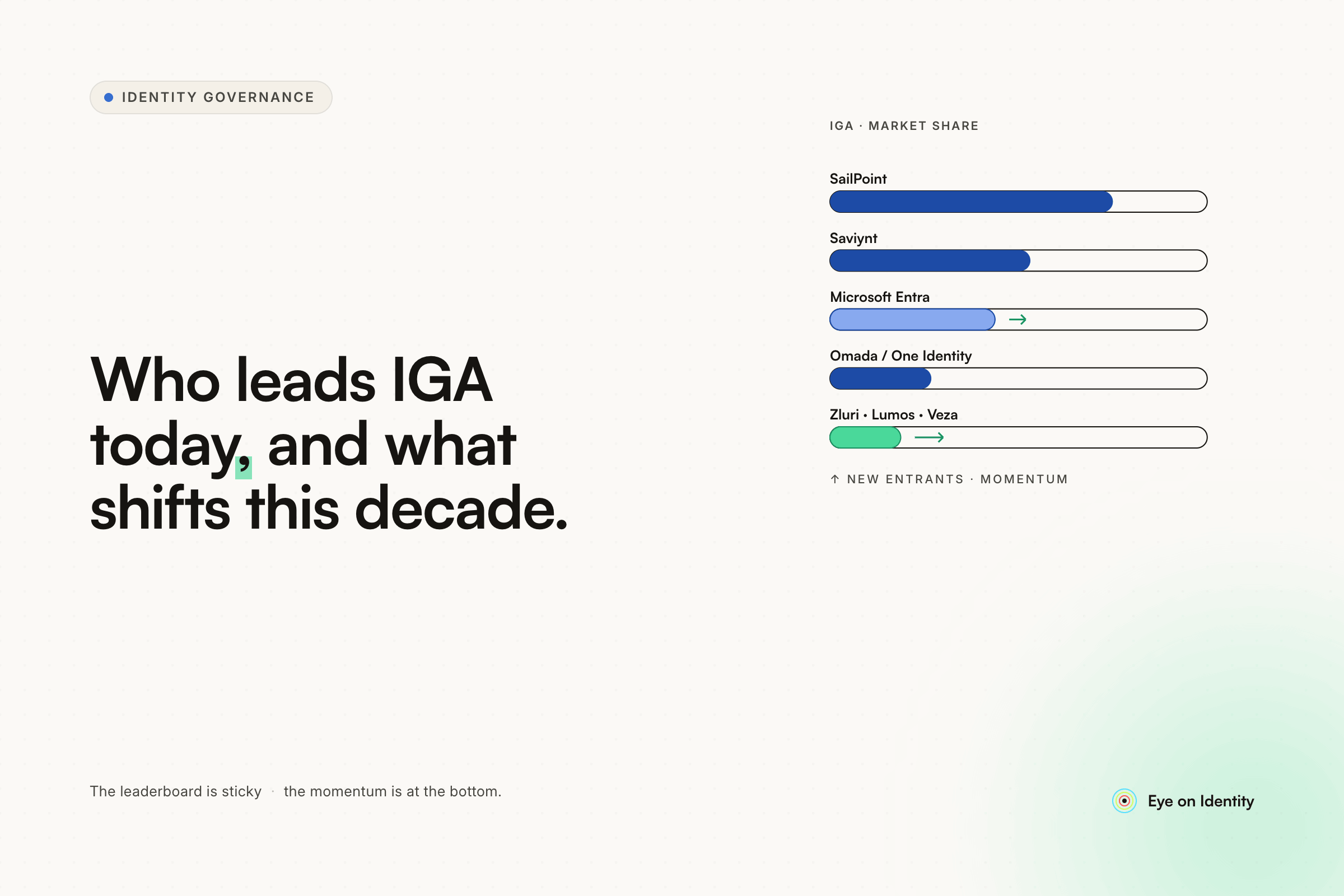

IGA: SailPoint leads, but the competition is real. SailPoint's dominance in enterprise IGA is genuine and acknowledged across the thread. It's built on deep enterprise implementations, a mature connector library, and the switching cost of ripping out IGA — which is considerable. Saviynt competes in the converged IGA plus PAM space and has cloud-native credentials. Omada is strong in Europe and consistently cited as a no-code-flexibility alternative to SailPoint's services-heavy implementation model. The thread debate between SailPoint and Omada advocates illustrates the real competitive dynamic: SailPoint is more powerful, more expensive, and requires more services spend to fully implement; Omada is more flexible to configure without coding, at a lower total cost.

Non-human identity: no clear leader yet. The NHI space — managing machine identities, service accounts, API keys, secrets, and non-human credentials — is fragmented and early. CyberArk's Venafi acquisition is the biggest move toward consolidating this layer, but the space has significant pure-play investment (Astrix, Oasis, Entro) with no dominant platform established. The practitioner consensus in the thread is that all current NHI solutions have meaningful capability gaps — this is the most open competitive layer in identity right now.

Where the Real Competition Is Happening: Mid-Market IGA

The enterprise IGA market — large organizations with complex governance, SoD requirements, and formal certification workflows — is relatively settled. SailPoint is deeply embedded. Ripping it out is expensive and disruptive. Incumbents tend to stay entrenched at that end of the market.

The competitive action is in the mid-market: companies with 200–2,000 employees who need real IGA capability — joiner-mover-leaver automation, access reviews that satisfy SOC 2 and ISO 27001, non-SSO app governance — but for whom SailPoint's implementation cost and services dependency are prohibitive. These organizations are underserved by the enterprise IGA incumbents and overserved by basic SSO providers.

This is where platforms like Zluri operate. The Okta IGA and Microsoft Entra ID Governance products are encroaching from the SSO layer, using existing customer relationships to expand into governance — the same pattern Microsoft used with Teams against Slack. But practitioners who have implemented both consistently note that the IGA extensions from SSO platforms are more expensive per capability and less purpose-built than dedicated IGA platforms.

The mid-market IGA question for buyers isn't "SailPoint or Saviynt" — it's whether the IGA capability built into their existing SSO platform is sufficient, or whether a purpose-built platform that handles the full JML lifecycle, non-SSO app governance, and access certification delivers better value at their scale.

The 10-Year View: What Actually Changes

The predictions from practitioners in this thread converge on a few consistent points.

Microsoft's position in workforce identity strengthens. Entra ID will be the default identity fabric for an increasing share of enterprise environments, and Microsoft will continue using that position to push Entra Governance capabilities into existing customers. The question isn't whether Microsoft grows its IGA footprint — it will — but whether its IGA product matures fast enough to displace purpose-built governance platforms for organizations with complex requirements.

Okta's position depends on what it does with IGA and whether it can maintain its integration advantage. The Okta IGA product (acquired from Atspoke) is newer than its SSO offering and carries the same feedback that Microsoft's governance product does — capable but expensive for what it delivers at mid-market scale.

SailPoint stays dominant at the high end of enterprise IGA. The switching cost is too high and the implementations too customized for significant churn. But their market growth comes from new enterprise customers, not from displacing existing ones, and the mid-market largely isn't served by their pricing model.

The IGA layer at mid-market scale remains the most open competitive space. Organizations that need governance beyond what their SSO provider delivers natively, but aren't large enough to justify a SailPoint implementation, represent a significant and growing buyer segment. Platforms that can deliver JML automation, non-SSO app coverage, access reviews, and audit trail documentation at a price point accessible to mid-sized organizations are well-positioned in this segment.

The longer-term structural shift noted in the thread — identity programs moving toward converged platforms that unify identity, application, permission, and usage data across both human and machine identities — is real but multi-year. The near-term competitive reality is that most organizations will continue running layered stacks (Microsoft or Okta for SSO, a dedicated IGA platform for governance, CyberArk or similar for PAM) rather than consolidating onto a single vendor.

What This Means for Buyers Evaluating IGA Today

The practical buying framework that emerges from this thread:

If you're a large enterprise with complex SoD requirements and budget for significant services spend: SailPoint or Saviynt are the realistic options. The implementation is substantial but the capability ceiling is high.

If you're in Europe or want no-code configuration flexibility at lower total cost: Omada is a credible alternative to SailPoint and worth evaluating seriously.

If you're Microsoft-heavy and your governance requirements are primarily within the M365 and Entra ecosystem: Entra ID Governance is worth evaluating as a native extension of your existing stack before adding a separate platform.

If you're mid-market, need real IGA capability across SSO and non-SSO apps, and want to avoid a services-heavy implementation: purpose-built platforms designed for this segment — including Zluri — address the gap that enterprise IGA vendors leave open at that scale.

The test one commenter recommended is worth running regardless of which vendor you're evaluating: ask them to show a complete access and usage timeline for a single identity with one query. It separates platforms with genuine data unification from those where the answer requires reconciling multiple systems manually.

Frequently Asked Questions

Which vendor dominates the IGA market in 2025?

SailPoint leads enterprise IGA by most measures — market share, analyst recognition, and depth of implementation in large organizations. Saviynt competes in the converged IGA plus PAM space. Omada is strong in Europe and mid-market. Microsoft Entra ID Governance and Okta IGA are expanding from their SSO positions. At mid-market scale, purpose-built IGA platforms serve organizations that need governance capability beyond what SSO providers offer natively but don't require the implementation complexity of SailPoint.

Will Microsoft Entra replace dedicated IGA platforms?

Microsoft will expand its IGA footprint using its M365 installed base, the same way it used Teams against Slack. Whether Entra Governance replaces dedicated IGA platforms depends on whether it closes the capability gap for complex governance requirements — SoD, non-SSO app coverage, and sophisticated access certification workflows. Current practitioner feedback is that Entra Governance is more capable than it was two years ago but still better suited for organizations already deeply embedded in the Microsoft ecosystem than as a general IGA replacement.

What is the difference between SSO and IGA?

SSO handles authentication — controlling whether a user can log into an application. IGA handles the governance layer above authentication: who should have access based on their role, how access is requested and approved, how access is reviewed periodically, and how access is revoked when someone leaves or changes roles. An organization can have excellent SSO and still have orphaned accounts, excessive permissions, and no audit trail for access decisions — which is exactly why IGA exists as a separate layer.

What IAM category has the least established market leader?

Non-human identity — managing machine identities, service accounts, API keys, and secrets — is the least settled category. CyberArk's Venafi acquisition is the biggest consolidation move, but the space has significant venture-backed pure-play investment with no dominant platform established. Most practitioners evaluating NHI tools report meaningful capability gaps across the current vendor landscape.

See How Zluri Fits Your IGA Stack

If you're evaluating IGA platforms for a mid-market environment and want to see how Zluri compares to extending your existing Okta or Entra ID setup, book a walkthrough specific to your stack — including non-SSO app governance and access certification that your SSO provider's IGA module may not cover.

.svg)