Understanding the critical differences between cost avoidance and savings is paramount. This distinction is the key to unlocking smarter financial decisions for IT managers and their businesses. Let’s delve into the differentiating factors of cost avoidance vs cost savings.

Many IT managers struggle to differentiate between cost savings and cost avoidance, which can lead to suboptimal financial decisions.

While cost savings bring immediate benefits by optimizing current financial positions and cash flows, cost avoidance focuses on mitigating potential future financial strains through risk management. Without a clear understanding of these concepts, businesses may fail to achieve long-term stability and resilience.

This guide will help you understand the critical differences between cost avoidance and cost savings, and how both strategies play indispensable roles in effective financial management. Let’s first explore what cost avoidance and cost savings are, and then delve into their distinguishing factors.

What is Cost Avoidance?

Cost avoidance refers to preventing costs that would otherwise be incurred if a particular action weren't taken. It involves identifying potential expenses or risks and implementing measures to circumvent or mitigate them. This concept is often employed in business and finance, where companies aim to prevent unnecessary spending by proactively addressing potential problems or inefficiencies before they occur.

Cost avoidance strategies can include measures such as optimizing processes, implementing better technologies, or avoiding risks that could lead to financial losses. Ultimately, it's about saving money by preventing expenses rather than dealing with them after they've occurred.

How to Calculate Cost Avoidance?

Understanding how to calculate cost avoidance is pivotal in proactive financial management strategies.

1. Cost Avoidance Calculation as an Amount:

Cost avoidance is a financial metric used to determine the savings achieved by implementing a proactive solution compared to the projected cost of inaction. Here's how you can calculate cost avoidance:

Projected Cost of Inaction − Cost of Proactive Solution = Cost Avoidance Savings Amount

Example: Suppose the projected cost of inaction is $50,000, and the cost of the proactive solution is $10,000.

Cost Avoidance Savings Amount = $50,000 - $10,000 = $40,000

The amount saved through cost avoidance is $40,000.

2. Cost Avoidance Calculation as a Percentage:

Projected Cost of Inaction − Cost of Proactive Solution = Avoided Cost

Avoided Cost/ Cost of Inaction = Cost Avoidance Savings Percentage

Example: Cost Avoidance Savings Percentage = ($40,000 / $50,000) * 100 = 80%

This indicates that by implementing the proactive solution, you've avoided 80% of the projected costs associated with inaction.

What is Cost Savings?

Cost savings refer to the actual reduction in expenses or spending compared to what was previously being spent. It involves finding ways to decrease expenditures within a business or personal budget without compromising the quality of products or services.

Cost savings can be achieved by negotiating better prices with suppliers, streamlining processes to reduce waste or inefficiencies, implementing more efficient technologies, or finding alternative, less expensive resources.

Unlike cost avoidance, which focuses on preventing potential expenses, cost savings are tangible reductions in actual expenditures. These savings can increase business profitability or allow individuals to allocate funds to other areas or investments.

IT companies often have specific initiatives or departments dedicated to identifying and implementing strategies for IT cost savings to improve their financial health and competitiveness in the market.

How to calculate cost savings?

Understanding how to calculate cost savings is pivotal in proactive financial management strategies.

1. Cost Savings Calculation as an Amount:

Calculating cost savings is indeed crucial in assessing the effectiveness of negotiations or procurement efforts. You can see how much money has been saved by measuring the difference between the initial proposed cost and the final contracted cost.

Initial Proposed Cost - Final Contracted Cost = Cost Savings Amount

Example: If the initial proposed cost was $10,000 and the final contracted cost is $8,000, the cost savings amount would be $10,000 - $8,000 = $2,000.

2. Cost Savings Calculation as a Percentage:

Expressing cost savings as a percentage can provide a different perspective, especially when dealing with various scales of expenses. Sometimes, a 5% savings on a large expenditure might represent a more substantial amount than a 10% savings on a smaller one.

((Initial Proposed Cost - Final Contracted Cost) / Initial Proposed Cost) * 100 = Cost Savings Percentage

Example: If the initial proposed cost was $10,000 and the final contracted cost is $8,000, the cost savings percentage would be (($10,000 - $8,000) / $10,000) * 100 = (0.2) * 100 = 20%.

These calculations provide valuable insights into financial efficiency and help make informed decisions for future negotiations or procurement strategies.

Benefits of Cost Avoidance

Embracing the practice of cost avoidance unlocks a multitude of benefits that transcend immediate savings, offering your teams a strategic pathway to financial resilience and operational excellence.

- Enhanced Profitability: Cost avoidance directly impacts the bottom line. By steering clear of unnecessary expenses, businesses can save resources and improve their profit margins without compromising quality or services.

- Operational Efficiency: Preventing unnecessary costs allows companies to allocate resources more effectively. Streamlining processes and focusing efforts on essential tasks saves time and money and improves overall operational efficiency.

- Competitive Advantage: Reduced expenses enable businesses to offer competitive prices to customers. This competitive pricing can be a significant advantage, attracting more customers and securing a stronger position in the market.

- Resource Allocation: Cost avoidance allows for better resource allocation. Funds and efforts that would have been spent on unnecessary expenses can be redirected to more critical areas such as innovation, research, or improving existing products/services.

- Risk Mitigation: Avoiding unnecessary costs can also mitigate risks. For instance, investing in preventative maintenance might prevent more significant repair costs down the line or avoid potential legal disputes by addressing issues early on, which can save substantial expenses.

Benefits of Cost Savings

Cost savings offer a multitude of benefits to businesses, from immediate financial gains to the creation of strategic opportunities for growth and investment.

- Immediate Financial Impact: Cost savings deliver tangible and immediate financial benefits. When a business reduces its operational expenses, it directly affects its bottom line. This means more money stays within the company, enhancing its financial health right away.

- Market Competitiveness: By effectively reducing operational expenses, businesses gain the ability to offer more competitive pricing while maintaining high-quality products or services. This enhanced competitive edge draws in new customers and retains existing ones, stimulating market expansion and sustained growth.

- Enhancing Profit Margins: Lowering costs directly boosts profit margins. For instance, if a company reduces its production costs, the difference between the selling price and the cost of production increases, leading to higher profits on each sale. This improved profitability strengthens the company's financial standing.

- Sustainability and Longevity: Cost savings strategies contribute to the long-term sustainability of a business. By being prudent with expenditures, companies create a more stable financial foundation for continued success.

- Creating Opportunities for Investments: The surplus funds generated from cost savings serve as a financial resource that can be strategically deployed. Businesses can use these savings to invest in various growth initiatives such as technological upgrades, market expansion, product innovation, or even talent development programs.

The Difference between Cost Avoidance vs Cost Savings

Exploring the differences between cost avoidance vs savings unveils strategies crucial for IT managers and their teams seeking to wield financial skill in today's dynamic and competitive landscape.

1. Proactive Approach VS Reactive Approach

Cost Avoidance: Cost avoidance is a proactive financial approach meticulously designed to predict and forestall potential future expenses long before they materialize. This strategy relies on foresight, strategic planning, and pre-emptive actions to mitigate or eliminate impending costs.

At its core, cost avoidance underscores the keen anticipation and prevention of future financial burdens. Companies deploying this approach conduct in-depth analyses of market trends, industry forecasts, and internal processes to pinpoint potential cost escalators. Once identified, they proactively take strategic steps to prevent these costs from denting their financial health.

Consider a manufacturing company navigating a volatile market where raw material prices are subject to erratic fluctuations. The company initiates negotiations with suppliers to anticipate potential price hikes in crucial raw materials. Through these negotiations, they lock in favorable and consistent prices for these essential resources. This proactive maneuver protects against future market price volatility, ensuring stable production costs and safeguarding the company's profitability.

Cost Savings: In contrast, cost savings strategies adopt a reactive stance, focusing on curbing existing and immediate expenses rather than precluding future ones. These strategies zoom in on identifying and executing measures to trim current expenditures without necessarily factoring in long-term consequences.

Businesses implementing cost-saving strategies optimize their financial standing by cutting operational costs or exploring more cost-effective alternatives for ongoing activities.

For instance, a retail store might leverage a cost-savings strategy by negotiating bulk purchase discounts with suppliers. By flexing their purchasing power, they secure better pricing for inventory, resulting in immediate cost reductions. This initiative directly impacts the current financial landscape by diminishing inventory expenses without fundamentally altering the underlying structure or processes of the business.

While cost avoidance vs cost savings contribute to financial prudence, they diverge in their temporal focus and approach. Cost avoidance prioritizes foresight and proactive measures to stave off future expenses, whereas cost savings zero in on swift reductions in current expenditures. Skillfully combining both strategies can fortify a company's financial resilience and sustainability in the long haul.

2. Hard cost savings VS Soft cost savings

Cost Avoidance: Hard costs encapsulate direct expenses tied to tangible assets. These expenses are usually associated with purchasing or acquiring physical items essential for business operations. Consider them the upfront, easily identifiable costs—such as buying inventory, equipment, land, or constructing facilities.

These expenses are explicit and easily quantifiable because they represent the actual, tangible value of the assets acquired. Hard costs are incurred at the time of purchase or construction, making them straightforward to estimate and record.

Cost Savings: In contrast, soft costs encompass indirect expenses related to intangible elements crucial for business functioning. These expenses are more abstract and challenging to quantify as they involve factors like legal fees, accounting services, banking charges, and other non-physical aspects of business operations. Soft costs are intricate to forecast because they often revolve around services or aspects that may not have an explicit monetary value attached or are difficult to measure precisely.

Soft savings denote the intangible benefits of continuous improvement and strategic measures within a company. Unlike hard savings, they aren't readily visible in financial records like invoices or receipts but manifest through capacity enhancements and measures that prevent costs. These savings play a critical role in overall business growth and efficiency, contributing to improvements that may not directly reflect on traditional financial documentation.

For instance, enhancing workplace safety, boosting employee and customer satisfaction, staying compliant with evolving regulations, and reducing the need for working capital are all examples of soft savings. While they might not have an immediate financial impact, they significantly contribute to the overall success and sustainability of the company in the long run.

3. Not directly reported in financial statements VS Reported on Financial Statements

Cost Avoidance: Indirect financial reporting involves strategies aimed at cost avoidance that aren't overtly displayed on financial statements but are crucially tracked within an organization. These approaches are often overseen by procurement, risk management, or strategic planning departments.

While they may not manifest directly on financial reports, their impact is substantial in maintaining operational efficiency and preventing potential financial setbacks.

For instance, consider a company prioritizing preventive maintenance protocols to evade expensive equipment breakdowns. Although these efforts might not translate into immediate financial gains or losses on the balance sheet, the success of these strategies is internally monitored through meticulous maintenance logs and comprehensive risk management reports.

By proactively managing equipment maintenance, the company avoids sudden, substantial costs that might otherwise arise from unexpected breakdowns, enhancing its overall financial stability.

Cost Savings: On the other hand, direct financial reporting revolves around initiatives that directly influence financial statements by visibly impacting current expenses and budgets. These initiatives, once implemented, bring about immediate and discernible changes in the financial reports and statements.

Take, for instance, a manufacturing plant that optimizes its production process, effectively reducing waste and operational inefficiencies. The direct result of this strategic decision is evident in the quarterly financial reports, showcasing immediate cost savings.

These savings stem from reduced expenditures on raw materials, enhanced operational efficiency, and minimized resource wastage, all of which reflect positively on the company's financial statements. This direct influence on the financial reports highlights the tangible impact of such cost-saving endeavors.

Both indirect and direct financial reporting strategies play pivotal roles in an organization's financial health. While indirect strategies may not be immediately reflected in financial statements, their proactive nature helps mitigate potential financial risks.

Conversely, direct strategies immediately impact financial reports, showcasing tangible and measurable outcomes in the company's financial performance. Both approaches are integral in maintaining an organization's balanced and resilient financial structure.

4. Predicts and estimates potential future savings VS Negotiations or actions undertaken presently

Cost Avoidance: Predictive nature in cost savings strategies encapsulates a proactive approach to financial management, leveraging foresight and analysis to anticipate and mitigate potential expenses. It's a multifaceted methodology that hinges on forecasting future expenses, taking calculated actions to avert these costs, and implementing immediate measures for tangible savings.

At its core, its predictive nature involves meticulously scrutinizing trends, market dynamics, and risk evaluations to forecast potential expenditures. This process isn't just about foreseeing costs but is also geared towards strategic investments or actions designed to counteract these foreseen expenses.

For instance, a retail chain might analyze market trends and anticipate a surge in raw material prices. To preemptively counter this, they might opt to secure bulk purchases at current rates or diversify suppliers to mitigate the impending cost hike, thereby ensuring future savings.

The predictive approach thrives on strategic decision-making, exemplified when companies anticipate future shifts or challenges and take proactive steps to curtail their impact on finances. Take the case of an automotive manufacturer foreseeing impending regulatory changes necessitating eco-friendly vehicle components. In anticipation, they invest in research and development to engineer these components, effectively evading potential fines or retrofitting expenses in the future.

Cost Savings: Contrasting this predictive strategy, immediate actions in cost savings strategies involve real-time interventions to reduce existing expenses promptly. These actions could range from renegotiating contracts and seeking better terms with suppliers to streamlining internal processes for greater efficiency.

For instance, a manufacturing firm might conduct an operational audit and identify redundant workflows. By promptly reorganizing these processes, they can swiftly realize reduced operational costs and bolster overall productivity.

In pursuing streamlined cost savings vs cost avoidance, SMPs have emerged as invaluable assets for businesses seeking to navigate the complexities of finance management.

Cost Avoidance vs Cost Savings Comparison Table

Here's a comparison table summarizing the key distinctions between cost savings vs cost avoidance. It outlines the distinct approaches, temporal focuses, impact on financial statements, nature of costs managed, and visibility in financial records between cost savings vs cost avoidance strategies.

Balancing both approaches, leveraging tools like Zluri, and understanding their nuances can significantly strengthen a company's financial position and resilience in a dynamic market.

How Zluri Helps with Cost Avoidance vs Cost Savings in Financial Management

Zluri's innovative platform revolutionizes the landscape of SaaS procurement, presenting a robust solution that transcends traditional methods, aiming at optimizing cost savings and proactive cost avoidance.

At the core of Zluri's offering lies a transformative approach to streamline software acquisition and renewal processes. This cutting-edge platform is meticulously designed to empower your IT procurement teams, enabling them to save substantial time and resources.

Zluri's holistic and forward-thinking approach to SaaS procurement holds a new era in cost management. It's a solution that unlocks immediate cost efficiencies and fortifies businesses against future financial strains, making it an indispensable tool for those seeking comprehensive, efficient, and forward-looking strategies in software procurement.

Zluri's impact on significant savings stems from its standardized SaaS procurement process, fostering collaboration among procurement, finance, and individual requesters. This meticulous approach ensures unparalleled transparency throughout the SaaS buying journey.

Maximizing Cost Efficiency With Zluri’s SaaS Buying Process

The platform's four-step SaaS buying process is a blueprint for efficiency and cost-effectiveness. Beginning with the discovery phase, Zluri's experts collaborate closely with the IT team. This phase stands out due to Zluri's utilization of five distinct discovery methods embedded within the platform.

These methods, encompassing SSO, finance, and expense management systems, allow for a comprehensive understanding of the organization's SaaS stack.

Zluri's SaaS procurement process unfolds in four meticulously structured steps, each designed to maximize cost efficiencies and streamline your software landscape:

Step 1: Discovery

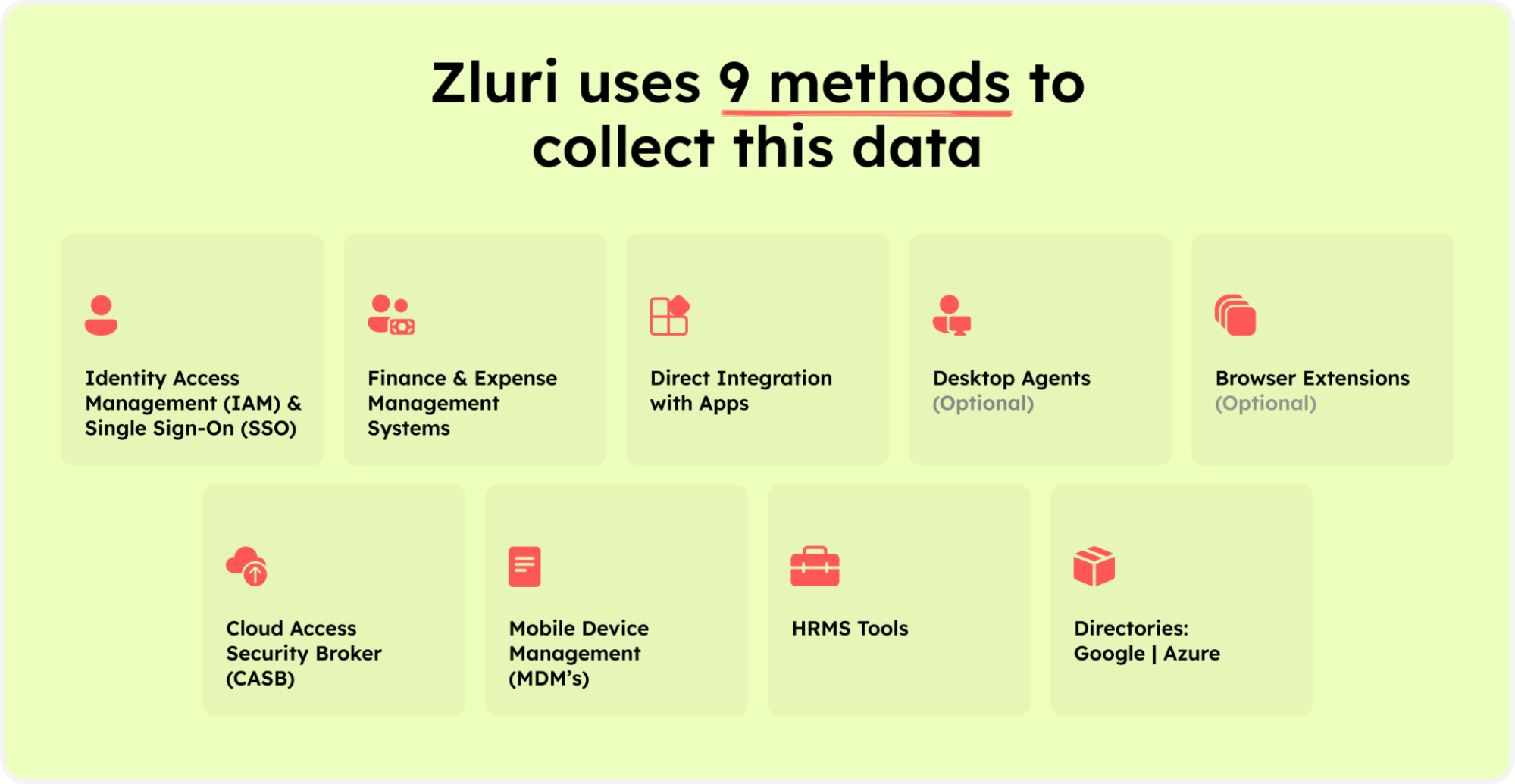

Zluri initiates this crucial phase by leveraging its sophisticated SMP to delve deep into your organization's SaaS technology. Collaborating closely with your team, Zluri ensures a comprehensive mapping of your SaaS stack using its platform, leaving no stone unturned.

Zluri employs nine discovery methods. These methods range from MDMs, IDPs & SSO, direct integration with apps, finance & expense management systems, CASBs, HRMS, directories, desktop agents (optional), and browser extension (optional).

Zluri’s nine discovery methods

Consider a multinational corporation with various departments using a multitude of applications. Zluri's discovery phase reveals that several teams across different regions use similar software for distinct purposes. This discovery allows for potential consolidation and significant cost reductions.

Step 2: Management

Efficient SaaS stack management is pivotal, and Zluri excels in this domain. The platform aids in eliminating redundancy and duplicates within applications, ensuring proactive management of auto-renewals, and optimizing license tiers. This meticulous management eradicates shadow IT practices and fine-tunes your SaaS spending, resulting in substantial savings.

Zluri identifies multiple redundant subscriptions within the organization, allowing for the elimination of overlapping software. This consolidation streamlines workflows and saves costs by ensuring resources are allocated to the most effective tools.

Step 3: Consolidation

Zluri's approach involves understanding your yearly purchase and renewal plans and consolidating this data within its SMP platform alongside your procurement history. This holistic view empowers Zluri to assist in planning your SaaS purchases for the upcoming 12 months, streamlining your procurement process and enhancing strategic decision-making.

By analyzing previous spending patterns and future needs, Zluri assists in creating a coherent SaaS purchasing plan. This strategic approach helps in negotiating better deals and budgeting effectively.

Step 4: Savings

The pinnacle of value in Zluri's process lies in the savings phase. Here, your teams or departments select the necessary tools, and Zluri takes the reins to negotiate optimal prices successfully on your behalf. Leveraging ZOPA (zone of possible agreements), Zluri's SaaS buying experts gauge the maximum price acceptable to you for an application.

Moreover, the platform harnesses the power of BATNA (best alternative to a negotiated agreement), meticulously evaluating various pricing options to select the most suitable one. Zluri further maximizes savings by automatically identifying and eliminating unutilized licenses or duplicate apps from existing subscriptions, ensuring cost efficiency across the board.

Zluri negotiates with vendors for better subscription rates, resulting in considerable cost savings while maintaining the necessary software resources for each department.

Through this meticulous and collaborative approach, Zluri optimizes your SaaS spending and enhances operational efficiency, unlocking substantial savings for your organization.

Transforming Cost Efficiency With Zluri’s Procurement Approach

Zluri goes beyond procurement to meticulously handle closure processes, encompassing legal, security, and financial checkpoints, while documenting each contract. This meticulous approach ensures compliance and provides a transparent monitoring system for your SaaS applications, actively averting potential legal or financial pitfalls and contributing to effective cost avoidance.

At the core of Zluri's service is its risk-free SaaS procurement model. You pay only upon Zluri delivering at least double the savings it costs, showcasing a commitment to substantial cost reductions and fostering a proactive financial culture.

Leveraging a profound understanding of the SaaS market, Zluri tailors SaaS stacks within allocated budgets, often yielding up to 50% savings on subscriptions. This immediate and substantial cost reduction optimizes resource utilization without compromising quality, a testament to Zluri's expertise in driving immediate cost efficiencies.

Moreover, Zluri's engagement spans 12 to 18 months beyond immediate benefits, establishing robust governance over SaaS contracts, negotiations, and payments. This forward-looking strategy ensures sustained efficiency and cost-effectiveness, proactively mitigating unnecessary expenditures and fortifying your organization against potential financial risks.

Zluri's proactive measures and strategic planning deliver immediate savings and secure enduring financial stability for your organization.

To boil it down, the comprehensive approach, combining predictive analysis and immediate intervention, makes Zluri an invaluable asset in achieving a balanced financial strategy that encompasses both cost avoidance and savings, ultimately bolstering an organization's financial health and resilience.

So what are you waiting for? Book a demo now.

Frequently Asked Questions (FAQs)

1. What is the fundamental difference between cost avoidance and cost savings?

- Cost Avoidance: It focuses on predicting and preventing future expenses through strategic planning and preemptive actions.

- Cost Savings: It involves reducing current expenses by immediate interventions and optimizations without necessarily considering long-term implications.

2. How can a business effectively balance cost avoidance and cost savings?

Integrating both strategies strategically: Using tools like data analytics for cost avoidance while implementing process optimizations or negotiations for immediate cost savings.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.webp)

.webp)

.webp)

.webp)