At the core of the Sarbanes-Oxley Act (SOX) is a fundamental pillar: Section 404(b). This section imposes a crucial responsibility on auditors: to evaluate and disclose a company's financial controls. By rigorously scrutinizing these controls, Section 404(b) safeguards organizations' financial integrity and transparency.

The Sarbanes-Oxley Act compliance presents challenges and opportunities for businesses, particularly those new to compliance. They need to keep up with changing rules and understand what Section 404(b) requires.

To address these complexities, it's imperative to delve into the intricacies of SOX 404(b) and chart out actionable steps for businesses to prepare and thrive.

Understanding SOX 404 Compliance

Sarbanes-Oxley Act (SOX) 404 compliance is a critical regulatory requirement for public companies that aims to maintain the integrity of financial reporting. It consists of two key provisions: Section 404(a) and Section 404(b).

What is Section 404(a)?

Section 404(a) mandates that management acknowledges and evaluates the effectiveness of internal controls over financial reporting. It underscores the importance of having reliable financial information to prevent fraud or errors in financial reports. This section requires companies to establish and maintain robust internal control mechanisms.

What is Section 404(b)?

Following Section 404(a), Section 404(b) involves external auditors in the compliance process. It requires external auditors to validate a company's internal controls over financial reporting through testing, inspection, or observation. This external validation ensures the reliability and accuracy of financial reporting beyond the company's internal assessments.

Let's focus on the intricacies of SOX 404(b) compliance, delving into its key components.

Key Components of SOX 404(b) Compliance:

- External Audit Verification: Under SOX 404(b), external auditors are tasked with independently assessing a company's internal controls over accounting activities. This involves testing procedures to ensure the effectiveness of these controls.

- Annual Review: Companies must undergo an annual examination wherein external parties verify the presence and functionality of internal controls. This process provides assurance regarding the accuracy and reliability of financial reporting.

- Transition from SOX 404(a): While SOX 404(a) focuses on establishing internal checks and balances, SOX 404(b) introduces the critical step of external audit validation. This transition emphasizes the importance of independent scrutiny in maintaining the integrity of financial reporting processes.

Which Organizations Must Be SOX 404(b) Compliant?

The Sarbanes-Oxley Act, section 404, mandates compliance for all publicly traded companies in the U.S. This includes wholly owned subsidiaries and publicly traded foreign companies conducting business in the U.S. However, SOX 404b compliance requirements vary based on the Securities and Exchange Commission (SEC) 's classification of filers.

Classification Criteria:

- Large Accelerated Filers

- Accelerated Filers

- Emerging Growth Companies (EGC) transitioning into Accelerated Filer status

Exemptions:

- Non-Accelerated Filers: The Dodd-Frank Wall Street Reform and Consumer Protection Act established an exemption to SOX 404b for non-accelerated filers, defined by the SEC. These companies are not obliged to engage an independent auditor for SOX testing and are only subject to the requirements of SOX 404a.

- Changes in SEC Definitions: The SEC updated its definitions of accelerated filer and large accelerated filer in March 2020, resulting in more companies becoming exempt from SOX 404b. Additionally, revisions to the definition of smaller reporting companies (SRCs) in June 2018 expanded the pool of exempt companies.

Criteria for Exemption Include:

- Smaller Reporting Companies (SRCs): Companies meeting specific financial thresholds (less than $250 million in public float or less than $100 million in annual revenues with less than $700 million in public float) and reporting less than $100 million in annual revenues in the most recent fiscal year are exempt.

- Emerging Growth Companies (EGCs): EGCs are exempt for the first five years following their initial public offerings if they meet certain criteria, such as not exceeding annual gross revenues of $1.235 billion, issuing less than $1 billion in non-convertible debt in the past three years, and not becoming large accelerated filers.

- Newly Acquired Businesses: Newly acquired businesses are exempt from SOX 404b requirements in the first year following acquisition.

SOX 404(b) compliance requirements vary depending on the Securities and Exchange Commission's (SEC) classification of filers, while SOX 404(a) serves as another crucial aspect of regulatory compliance.

Organizations can strategically plan their compliance endeavors by comprehending the distinctions between SOX 404(a) and 404(b). This ensures adherence to regulatory standards and promotes transparency in financial reporting practices. Let's delve into their differences:

Key Differences Between 404(a) vs 404(b)

Understanding the key differences between 404(a) and 404(b) is essential for navigating the Sarbanes-Oxley Act's compliance requirements.

1. Compliance Obligation

Both sections, 404(a) and 404(b), are integral components of the Sarbanes-Oxley Act. 404(a) focuses on establishing and maintaining internal controls, while 404(b) requires auditing these controls. These provisions apply to qualifying companies with over $75 million in public investor shares.

2. Regulatory Differences

404(a): Mandates rigorous internal control assessments by public companies, subject to external auditor scrutiny.

404(b): Tailored for smaller public companies, offering exemptions from external auditor attestation.

3. Use of Framework

404(a): Allows management flexibility in assessing internal controls without a specific framework requirement.

404(b): External auditors are required to use recognized IT security and privacy frameworks like COSO for attestation.

4. Compliance Requirements

404(a): Demands evaluation and external auditor attestation, adding an extra validation layer.

404(b): Offers a more adaptable approach, focusing on management-conducted internal control assessments.

5. Impact on Businesses

404(a): Imposes significant financial and administrative burdens, potentially hindering innovation and growth.

404(b): Provides flexibility, easing financial burdens for smaller companies while emphasizing internal controls.

6. Risk Management Perspectives

404(a): Ensures robust defense against financial risks but may divert focus from broader risk management.

404(b): Encourages internal control awareness but lacks external scrutiny, potentially leading to blind spots in risk assessment.

7. Timing

404(a): Requires continuous management assessment of internal controls quarterly and annually.

404(b): Involves annual external auditor attestation, providing a detailed evaluation within the annual reporting cycle.

Let's move on to the steps required for SOX 404(b) compliance preparation.

Steps for SOX 404(b) Compliance Preparation

Preparing for compliance with SOX 404(b) involves strategic planning and execution. Here are some essential steps to help you navigate the regulatory landscape effectively.

1: Assessment of Existing Controls

Conducting a review of existing internal controls is a critical step in preparing for SOX 404b compliance. Here's how you can approach this assessment:

- Document Controls: Gather documentation on existing internal controls related to financial reporting.

- Identify Key Processes: Determine the critical financial reporting processes in your organization.

- Evaluate Design: Assess if controls are designed effectively to address financial reporting risks.

- Assess Effectiveness: Review evidence to ensure controls are operating as intended.

- Identify Weaknesses: Pinpoint any weaknesses or deficiencies in controls.

- Assess Risk Impact: Evaluate the potential impact of control weaknesses on financial reporting accuracy.

- Prioritize Remediation: Focus on fixing high-risk control weaknesses first.

- Document Findings: Record assessment results and proposed remediation actions for compliance evidence.

2: Top-Down Risk Assessment

Initiate your compliance journey with a robust top-down risk assessment strategy. By delving into the core business objectives, this method enables an exploration of potential pitfalls in financial reporting.

Understanding the goals allows for pinpointing specific areas where financial inaccuracies or misstatements could arise. This facilitates proactive measures to mitigate risks.

This comprehensive approach ensures regulatory compliance and strengthens your organization's financial integrity. By systematically identifying and addressing potential vulnerabilities from the top down, you establish a solid foundation for sound financial reporting practices.

Also read: 9-Step SOX Compliance Checklist | Zluri

3: Documentation of Processes

Documenting processes entails capturing the procedures within your organization and detailing transaction flows from initiation to completion. It means identifying critical control points and specifying responsible individuals or departments. This documentation ensures clarity and accountability in executing and overseeing organizational access controls.

When you document processes clearly, it becomes easier to identify any weak spots or areas that need improvement. It also helps auditors check that everything is being done correctly, which is important for meeting regulatory standards like SOX 404b.

Therefore, by taking the time to document processes well, you're not just staying organized but also making sure your organization runs smoothly and meets its legal requirements.

4: Walk-Throughs & Testing of Controls

Engage in detailed walk-throughs of critical processes alongside relevant stakeholders. These sessions serve to validate that controls are not only adequately designed but also effectively implemented within the operational framework.

Potential gaps or inefficiencies can be identified and addressed early in the compliance process by involving key personnel.

Conduct testing of key controls to ascertain their operational efficacy. This multifaceted evaluation encompasses both manual testing methodologies and the utilization of sophisticated automated tools where applicable.

Through rigorous testing protocols, organizations can confidently ensure the reliability and accuracy of their control mechanisms, thereby fortifying their overall compliance posture.

5: Evaluation of Exceptions & Remediation Recommendations

Evaluate any exceptions or deficiencies uncovered during the testing phase with attention, analyzing their potential impact on financial reporting integrity. Determine the significance of these findings in relation to compliance requirements and overall business operations.

Subsequently, craft detailed remediation plans tailored to address the identified issues effectively. These plans should outline specific actions to rectify deficiencies, bolster existing controls, or introduce new control mechanisms where warranted.

Consider implementing process improvements alongside control enhancements to fortify the organization's internal control environment.

Your organization can proactively mitigate risks by incorporating remediation strategies based on thorough testing and evaluation. This strengthens its adherence to regulatory standards and fosters greater financial transparency and trustworthiness.

6: Key Controls Identification

Thoroughly identifying key controls is crucial for effectively operating your internal control system. By pinpointing these critical controls, you can prioritize testing efforts to ensure they are robust and effectively mitigate risks to financial reporting.

This entails analyzing the significance of each control in mitigating risks and considering its impact on financial statement accuracy, regulatory compliance, and overall business objectives. Through this systematic approach, you can allocate resources strategically, optimizing the efficiency and effectiveness of your compliance efforts.

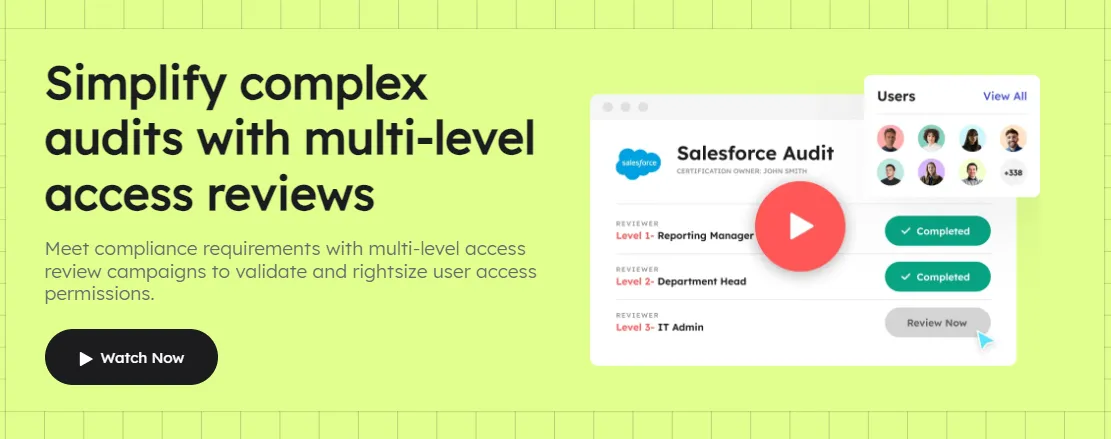

7: Implementation of an Access Review Solution

Companies must undergo compliance audits of their internal controls to comply with SOX Section 404(b). Access review solutions are essential for ensuring the effectiveness and integrity of these controls and facilitating compliance with SOX's regulatory requirements.

Zluri's advanced access review solution is tailored in adherence to SOX compliance. SOX 404(b) requires companies to have effective processes for reviewing and testing internal controls, including access controls.

Zluri's automation in access review processes ensures efficiency and accuracy in assessing access controls, which is essential for demonstrating compliance with SOX requirements. In fact, KuppingerCole's analysis reveals that Zluri's automated access remediation and entitlement control policies allow access reviews to be finished in days instead of weeks or months.

- Automated Access Certification Excellence: SOX 404(b) compliance mandates regular assessment and certification of internal controls, including access controls. Zluri's automated access certification feature simplifies this process by automating the review and certification of access controls, ensuring compliance by regularly verifying and certifying access rights.

- Segregation of Duty (SoD) Policy: SOX compliance underscores the necessity of segregating duties to prevent conflicts of interest and fraud. Zluri implements SoD policies and procedures to ensure that users cannot simultaneously hold conflicting roles, thereby strengthening internal controls and aligning with SOX requirements.

For example, a user responsible for approving expenses should not also be responsible for initiating payments. - Real-time Alerts and Notifications Precision: SOX compliance demands timely identification and remediation of control deficiencies or unauthorized access.

Zluri's real-time alerts provide immediate notifications of conflicting roles or suspicious activities, empowering organizations to address compliance issues as they arise proactively.

For instance, if a user attempts to access sensitive financial data without proper authorization, Zluri alerts the compliance team for immediate action. - Precision with Scheduled Certification Features: SOX compliance necessitates periodic assessments and certifications of internal controls. Zluri's scheduled certification feature enables organizations to conduct periodic user access reviews based on predetermined criteria. This ensures that access controls are consistently evaluated and certified in accordance with SOX requirements.

For instance, organizations can schedule quarterly access reviews to verify that employees have appropriate access levels based on their job responsibilities.

Book a demo today to Experience Zluri's capabilities firsthand. See how our advanced access review solution streamlines control assessments and ensures compliance with SOX 404(b) requirements.

Now, let’s take Datadog as an example to see how you can automate access review in Zluri.

Strengthening Financial Integrity with SOX Section 404(b) Compliance

Section 404(b) of the SOX Act helps ensure companies are honest about their finances. It requires them to have yearly checks of their internal controls to prevent fraud.

By following these rules and having strong controls in place, companies can make investors and others trust that their financial reports are accurate. This helps companies stay transparent and accountable.

FAQs

1: What are the potential consequences of non-compliance with Section 404(b)?

Non-compliance can result in financial penalties, loss of investor trust, increased regulatory scrutiny, and reputational damage to the company.

2: How does compliance with Section 404(b) contribute to financial transparency and investor confidence?

Compliance with Section 404(b) ensures that companies have robust internal controls, which enhances the accuracy and reliability of financial reporting. This transparency fosters investor confidence and strengthens trust in the integrity of the financial markets.

3: What differentiates Section 404(b) from Section 404(a) of the Sarbanes-Oxley Act?

While Section 404(a) mandates companies to establish and maintain internal controls, Section 404(b) specifically requires external audit validation of these controls.

.svg)